5 Emerging Benefits Trends to Look for in 2025

As 2024 comes to a close, HR professionals must rethink benefits strategy going into next year. This past year has been shaped by major financial uncertainty and advancements, influencing the benefits trends going into next year. All of these factors mean that employee needs are changing. Your current benefits need to keep pace.

The common theme emerging from this year’s insights is personalization. Employees want solutions to their unique problems – from building retirement savings to handling unexpected medical expenses. Compared to years prior, employees want more retirement benefits and paid leave opportunities. Financial wellness remains at the forefront of worker attention.

Here are the most important benefits your company needs in 2025.

Financial wellness remains atop the benefits trends

The common thread that connects most employee concerns is a high level of financial stress. Money worries continue to strain employees across all job sectors, income levels and generations. The stress is due to multiple factors, including an increased cost of living, especially among rent and groceries prices, over the past few years. According to CNBC, heightened expenses have led to the most common financial milestones, (such as retiring, purchasing a home or vehicle, and getting married) becoming out of reach for a significant population.

With a dedicated financial wellness program, you can help employees manage their finances — reducing stress and improving productivity. Financial wellness programs offer customized resources that provide essential information — regardless of age or income level.

According to Mercer’s Survey on health & benefit strategies for 2025, almost 70% of surveyed companies offer or plan to offer financial wellness programs in their benefits package next year. This projection shows the benefits trends in use and utilization of financial wellness programs among employees.

Focus on personalized benefits first

Personalized benefits put your employees in a position to succeed. Your employees have different struggles based on their age, experience and financial history. The right benefits package needs to cater to the unique needs of your workforce. This applies to new college graduates and senior employees alike. Employees who feel their benefits match their situation feel more loyalty to their company.

As technology improves, personalized benefits will be able to cater to a person’s exact struggles. New opportunities appear every year. In SHRM’s 2024 Employee Benefit Survey, menopause benefits, gender-affirming care and lifestyle savings accounts trend for the first time. However, even as new benefits appear, the core goal will remain the same — offering solutions that enhance individual lives.

Inclusive health benefits are still widely sought after

Medical costs continue to be a major concern for employees going into 2025. Almost half of Americans surveyed by the Commonwealth Fund have had surprise medical bills they expected to be covered by insurance. This added stress can drastically affect an employee’s finances, especially if they do not have an adequate amount saved — and now, companies require solutions.

Companies help employees make their healthcare costs more manageable through effective healthcare benefits. According to Mercer’s Survey on Health and Benefits Strategies for 2025, about two-thirds of large employers said that “improving healthcare affordability” is a priority for the next year. One method of support employers provide will come in the form of affordable deductibles. According to the report, 40% of large companies will offer a medical plan with a low or no deductible.

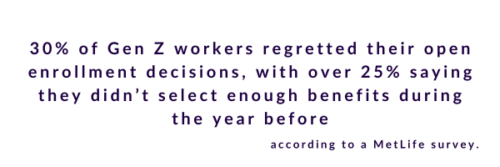

Retirement benefits trends may help move the needle

In SHRM’s Employee Benefits survey, more than 80% of employers said that retirement benefits were “very” or “extremely” important. These benefits trends will continue going into 2025.

The average employer matches 6% of an employee’s Traditional 401k and Roth 401k contributions. However, planning for the future continues to be a major stressor for employees. According to a 2024 PlanAdviser survey, 48% of employees claimed that concerns about their retirement savings were the top cause of their financial stress. Additionally, 62% of employees in the survey noted that retirement plans contributed the most to their financial security, which was up from 56% in 2023.

Creative solutions (such as student loan debt assistance and tax-advantaged health savings accounts) may be the key to supplementing your current retirement benefits.

Flexibility improves productivity

Flexibility in benefits packages comes in many forms — from remote/hybrid schedules or inclusive leave opportunities. In March of 2024, 11% of private industry workers had access to flexible benefits, which allowed employees to customize their packages as needed. According to Plan Adviser, interest in paid leave increased by about 15% from its figure in 2022.

Remote and hybrid work also continue to hold as a popular option for employers and employees. According to The US Bureau of Labor Statistics, productivity in 61 industries increased when employees switched to remote work. Research from Forbes also found that 98% of employees want to work remotely and project 32.6 million employees will be remote by 2025.

Providing a working environment where employees can be the most productive is crucial to flexible compensation packages. The ability to use benefits as they see fit also improves retention among your workforce.

Looking for the right financial wellness program to round out your benefits for 2025?

Best Money Moves is an AI-driven, mobile-first financial wellness solution designed to help employees with varying levels of financial knowledge dial down their most top-of-mind financial stresses. As an easy-to-use financial well-being solution, Best Money Moves offers comprehensive support toward any money-related goal, ranging from debt management to purchasing a home. With 1:1 money coaching, budgeting tools and other resources, our AI-driven platform is designed to help bolster employee financial wellbeing.

To learn more about Best Money Moves Financial Wellness Platform, let’s schedule a call. Contact us and we’ll reach out to you soon.