Mastering the High Stakes Benefits of Employee Financial Wellness

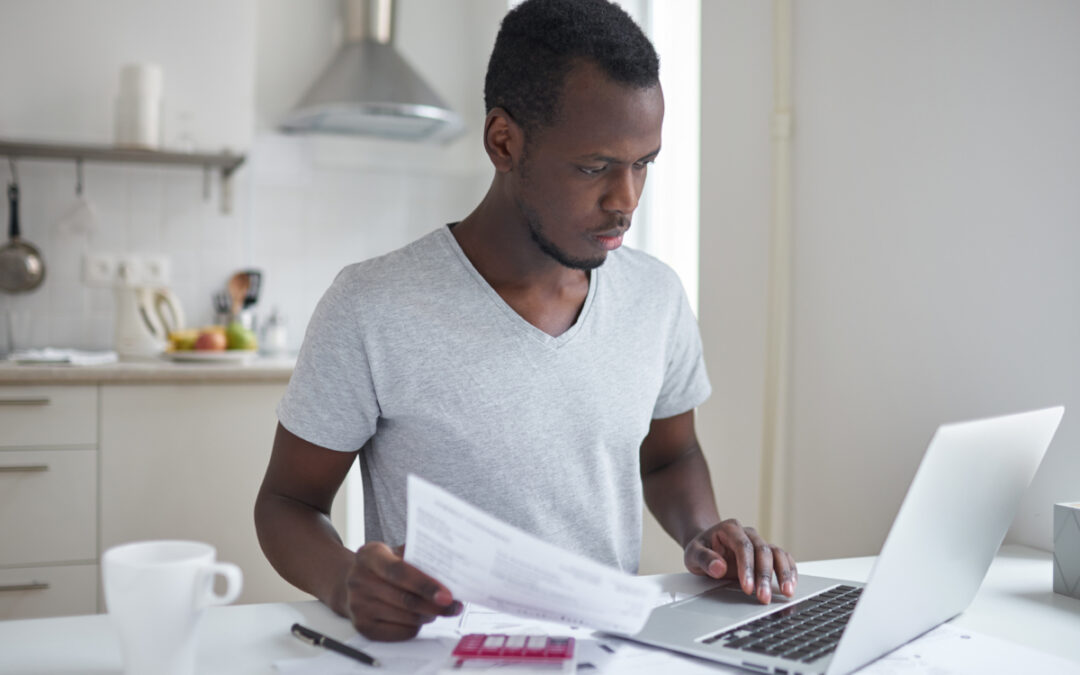

More employers recognize that financial wellness is table stakes for employees. What has also become apparent is that simply providing a 401(k) and retirement planning advice isn’t enough to reduce the financial stress almost all employees feel. Your employees need more.

Many employees struggle with paying down debt. They often have significant, unreimbursed, medical expenses or may be experiencing other financial hardships. This means they don’t always have the option to set aside funds for retirement, and have to “opt-out” of employer-sponsored savings plans simply because they can’t afford it..

From the employer’s point of view, adding one more benefit to an increasingly expensive pot might seem like a waste of money, especially if the employee benefits you’re providing aren’t being fully utilized.

But when it comes to financial wellness, the calculus is different. Forty-nine percent of employees feel that their workplace productivity would increase if their employer-sponsored benefits included financial planning programs in addition to existing retirement savings assistance. While retirement planning benefits are important, they don’t come close to capturing the full financial wellness needs of your workforce. Employees with financial security are much more motivated and focused at work.

In this week’s blog post, we run down the reasons that:

Financial Wellness Is About More Than Just Retirement Planning Advice

Do you feel like workplace financial wellness is out of reach? Ideally, financial wellness programs will lower health costs, enhance productivity, boost employee engagement and reduce employee absenteeism and turnover. Often, the only barrier is getting employees to try something new.

How to improve workplace financial wellness

Is your onboarding process thorough enough? If your onboarding process goes beyond basic training to include “acculturation,” then it probably isn’t. Whether it’s for new hires or internal transfers, when you consider the amount of time, staffing and money that goes into your onboarding process, shouldn’t it be fully comprehensive?

The importance of expanding your onboarding process – across the board

Positive investments in small businesses is driving economic growth. Small business investments continued to grow at the end of 2017 as payment delinquencies and defaults remained low. However, some warning signs in financial health are starting to emerge.

Small business investments – what you need to know

How do you know if your corporate wellness program is successful? The answer is much more nuanced than simple numbers and charts although those are important as well. Beyond standard metrics, a successful program will show employees with more energy, enthusiasm, productivity, creativity, higher engagement and lower absenteeism.

Here’s why financial wellness goes beyond numbers

The Tax Cuts and Jobs Act has altered two important tax breaks for homeowners. Homeowners with large mortgages and home equity loans should be paying attention to the new tax laws, as there are new limits on deductions for state and local taxes. There are fine details that you should read about to see how they’ll affect you – and your employees.

The new tax law may affect you more than you think

Is there a magic number that tells you how much to save for retirement? Or a magic 8-ball that tells you what to do with your retirement investments when the market drops? Unfortunately, magic won’t help you save for retirement. But, planning, saving, thinking outside of the box, doing a lot of research and speaking with an expert just might.

Your retirement savings goes beyond a market dip

Have something to add? Email info@bestmoneymoves.com.