Updated September 19th, 2019: The Best Money Moves Team is heading to HR Tech and SAP’s SuccessConnect in Las Vegas. Will you be attending either of these events? If so, please stop by and say hello. We’d love to show you our Best Money Moves financial wellness solution and explain why we’re winning awards, closing deals and making employees everywhere smarter about money.

The Best Money Moves team is headed to HR Tech and SAP’s SuccessConnect. While we’re en route to Las Vegas, I’d like to share with you why I started Best Money Moves, a mobile-first, cloud-based technology + coaching platform designed to help people measure their level of financial stress and dial it down in order to get control of their financial lives.

I’m a longtime financial journalist, syndicated columnist, book author and radio talk show host. I’ve been helping people make smarter decisions with their money for more years than I care to count! Five years ago, I was hired by three different companies to design financial wellness programs. Their intent was to create an opportunity to sell their own services by giving a veneer of financial education to employees.

Given that we were in the aftermath of the Great Recession, I didn’t think that would work. And, it didn’t. None of the companies wound up creating a successful product because the truth was – and is – that the majority of employees are broke.

How broke? Forty percent don’t even have $400 in cash for emergencies, and less than 75% don’t have $15,000 saved in a 401k. In my book, that’s pretty broke.

One day, I had an insight that would change the trajectory of my career – which up until then had been spent as a financial journalist and the owner of a content production company specializing in financial information.

I realized that financial wellness companies fall into a couple of categories:

-

- Niche products. These try to solve student loan problems for Millennials, or they claim to help you save for retirement by taking the change from a cup of coffee (which you shouldn’t be buying) and socking it away somewhere or helping you earn a little more interest on your savings, or they help you get paid faster, sometimes by the end of the day so you don’t have to get a payday loan.

- Products that try to sell you things. Like the products I was asked to design, these push credit cards, loans, different types of insurance and other things that most employees don’t need and can’t afford.

- Financial education products. These are typically course-based and require employees to do a lot of general learning about money before they can figure out how to solve their problems.

- Products that try to get assets under management. These tell you all about saving for retirement, and encourage you to get into their robo-investing platforms with whatever cash you have available.

Here’s my insight: No one was attacking the problem from the perspective of the employee: They’re extremely stressed about money and have pain points they want to solve now. And, they need help.

So, what if we designed a program that would help the employee understand the root cause of their financial stressors (because, there’s always more than one), use algorithms and machine learning (you know, the cool stuff) to push relevant, personalized information and solutions? What if we helped employees solve the financial problems they have today, across a wide spectrum of issues? Everything from student loans and credit card debt to identity theft, marital issues and elder care?

And, what if we let employees drive it?

Best Money Moves is my answer to the problem of employee financial stress. I know it has a huge ROI for employers, whether you’re trying to measure the effect of financial stress on healthcare costs and outcomes or retention or workplace accidents or unexplained absences. (Our technology can be used to measure all of these issues, and more. Just ask us how.)

Having spent a long career helping people make smarter decisions with their money, I knew there was a better way to help. So, we created a mobile-first platform that is simple to use, easy to understand, yet provides a great depth of knowledge across a wide spectrum of issues. And, we used the latest tech tools so the product would be smart enough to be personalized and relevant. And, we offered employers real-time metrics so they would have the same wonderful experience that they were providing to their employees.

Best Money Moves came out of beta in 2017 and has been winning awards, customers and accolades ever since.

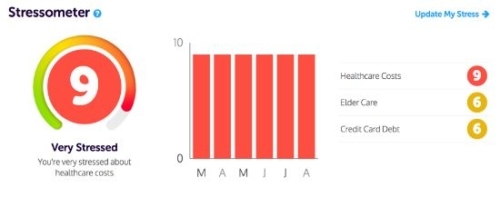

Financial wellness is getting a lot of attention these days, but wherever we go, CEOs, CHROs, and CFOs are fascinated by the Best Money Moves Stressometer™, which is our primary financial stress assessment tool. We break down financial stress into 14 categories and use interactive algorithms to delve deeper and identify the root causes of someone’s financial stress.

The Stressometer™ is just one tool that differentiates Best Money Moves from other financial wellness services. We also have 540 original pieces of objective, custom-created content: video, written articles, calculators and other tools. We’re gamified, with contests that carry cash prizes. We allow our customers to customize Best Money Moves to an incredible degree – because each company is different, and we want to support their company culture.

And, it’s working. Financial stress levels are starting to go down for our customer’s employees. It’s not a magical overnight experience: Financial stress is real, and does more than keep your employees up at night so they’re less productive during the day. But for those employees using our product, they’re finding relief. And, that’s just the beginning of the ROI that companies enjoy.

As Founder/CEO of Best Money Moves, I’m proud that we’re helping people reduce their level of financial stress. We’ve figured out how to help your employees understand their finances better, dig their way out of debt, and feel more empowered to handle the everyday money issues they face.

So, if you’re at SAP SuccessConnect or if you’re attending the 2019 HR Technology Conference in Las Vegas stop by the Best Money Moves at booth #2550 to say hello and learn how you can bring financial wellness to your company in 2020.