3 Digital Tools That Can Help Boost Employee Wellness

Whether your team is remote or heading back to the office, digital solutions can make it easier for your team to get the benefits they are eligible for. Companies have been turning to online tools to improve the reach and accessibility of employee wellness benefits.

Here are 3 digital tools that can boost employee wellness.

Across the globe, workforces have integrated digital wellness tools into their employee benefits offerings. The specifics of these tools vary depending on the company. However, these digital benefits can provide well-being support, at unprecedented levels of accessibility.

1. Financial wellness apps

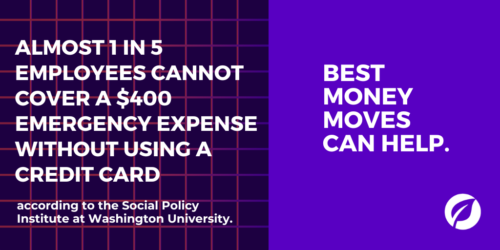

Financial stress can worsen a person’s physical and emotional health and even work productivity. In fact, according to PwC, 49% of financially-stressed employees said their money worries had a severe impact on their mental health. Yet, despite the abundance of employees who are financially stressed and want help, 41% are embarrassed to seek help with their finances.

To make financial support more accessible and approachable, many companies have turned to digital financial wellness solutions. From budgeting apps to AI-driven money software, digital financial wellness tools allow employees to budget, save, and more — on their own time, all from their mobile devices.

2. Meditation and fitness apps

It can be challenging to balance work life while tending to your mental and physical health. To help employees dial down their anxiety and stress, whether personal or work-related, companies have started offering free memberships to meditation and fitness apps.

Meditation apps allow employees to tend to their mental and emotional wellness, when and wherever they feel the most comfortable — this can be at home, on their commute to work, or even after a stressful meeting.

Moreover, studies have shown that physical outlets can help reduce stress and anxiety, so investing in fitness apps not only boost employees’ physical health but their emotional and mental health too.

3. Online talk therapy

Looking deeper into Biden’s plan, the administration is vying to change how people repay their loans. For example, the administration has proposed that borrowers pay 5% of their income each month in repayments, compared to the previous 10%.

In addition, the Department of Education proposed a rule to cover a borrower’s unpaid monthly interest, as long as they make their monthly payments. This is to curtail the exponential growth of loan balances, due to compounding interest fees. With a financial advisor, employees can learn how to navigate these changes and understand what they may mean for their financial situation.

Does your workforce need a financial solution for employee wellness? Try Best Money Moves!

Best Money Moves is a mobile-first financial wellness solution designed to help dial down employees’ most top-of-mind financial stresses. As a comprehensive financial well-being solution, Best Money Moves offers 1:1 money coaching, budgeting tools and other resources to improve employee financial wellbeing. Our AI platform, with a human-centered design, is easy to use and fit for employees of any age, right from their mobile phones.

Whether it be college planning or securing a mortgage, Best Money Moves can guide employees through the most difficult financial times and topics. Our dedicated resources, partner offerings and 700+ article library make Best Money Moves a leading benefit in bettering employee financial wellness.

To learn more about Best Money Moves Financial Wellness Platform, let’s schedule a call. Contact us and we’ll reach out to you soon.