2024 Employee Benefits Trends: Focus on Employee Wellbeing

Employee benefits are a driving force keeping your workforce satisfied. A study from the Society for HR Management found that the quality of employee benefits was likely linked to happiness at work. Yet both benefits and job satisfaction were at historic lows in 2023, falling multiple percentage points from the previous year.

A new year means revisiting your existing benefits strategy and experimenting with new programs to help keep your team engaged.

4 Top 2024 Employee Benefits

1. Financial wellness programs

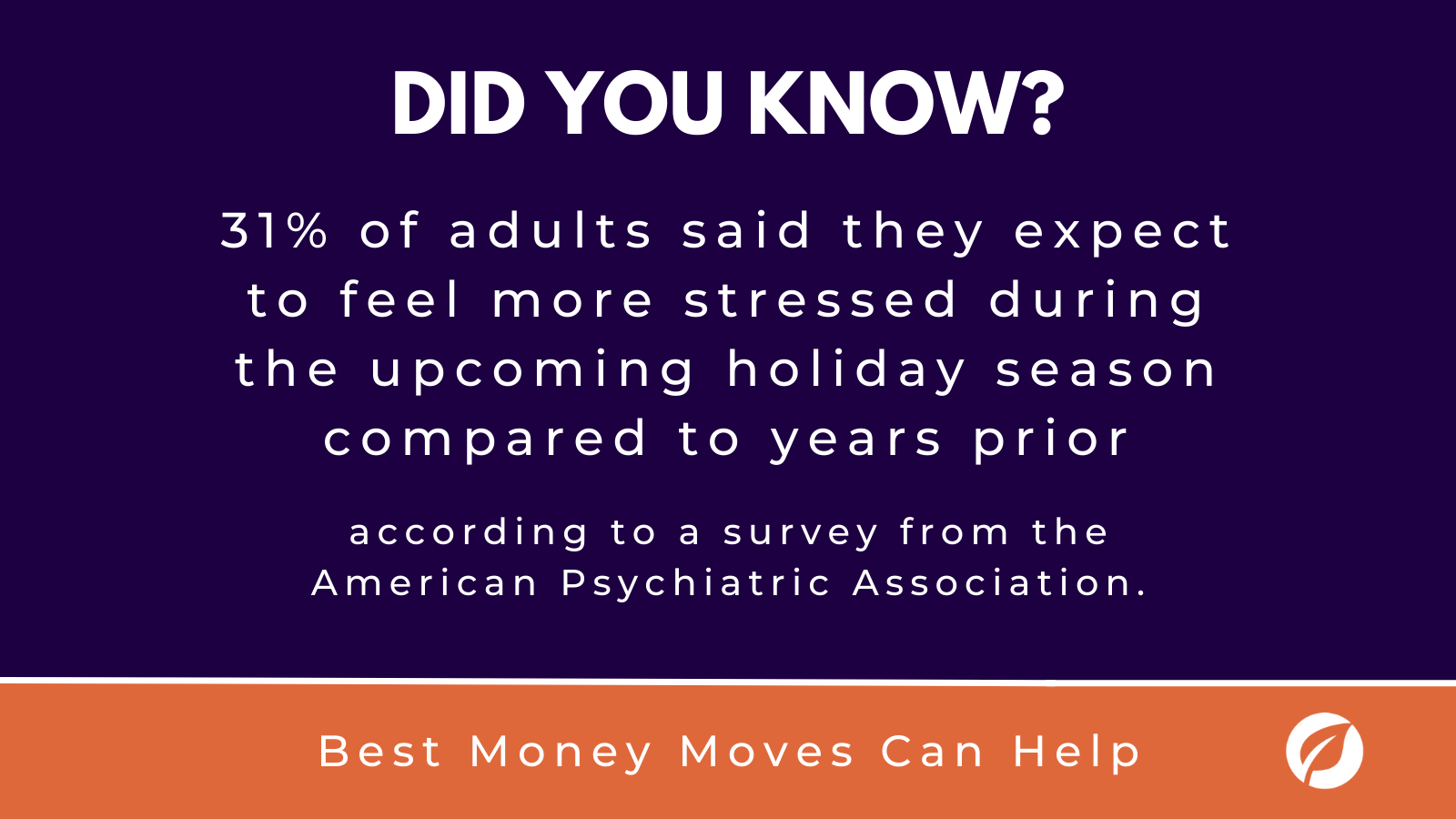

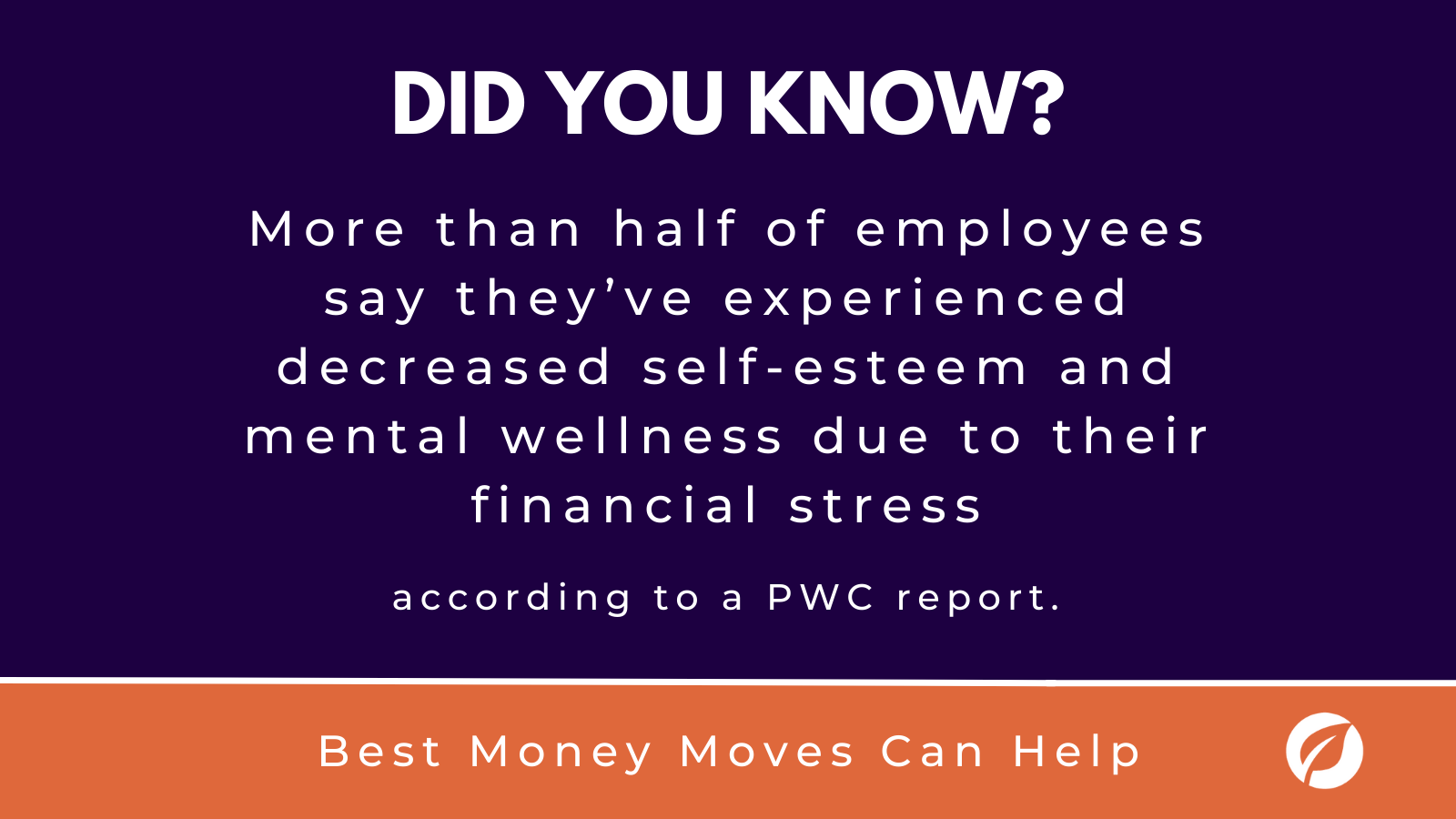

Financial health is one of the most important aspects of employee well-being and productivity. A study from the American Psychological Association (APA) found that 72% of Americans report stressing about money at least some of the time. According to Morgan Stanley, financial stress in employees can lead to declines in productivity, weakened company culture and delayed retirement, among other risks.

The answer is to meet employee financial strain head-on by providing a comprehensive financial wellness program in your 2024 employee benefits.

Financial wellness programs are expanding to include personalized financial planning, budgeting tools and educational resources. Other opportunities include student loan assistance, debt management programs, and employee assistance programs that provide financial counseling. Offering a wide range of interactive benefits helps employees. Budget tools can help save money for retirement, while debt management programs can help get a person’s situation back on track.

Mercer’s Health & Benefit Strategies for 2024 Survey Report found that almost half of surveyed employees believed digital tools would be useful to self-manage their well-being. Addressing the financial issues facing your workforce that their workforce faces can positively the lives of your team.

2. Flexible work schedules

Flexibility in scheduling continues to matter to employees moving into 2024, as companies recognize the value of work-life balance. The pandemic has shown the world that juggling work and family obligations is extremely difficult. But this reality is not just a pandemic-era issue. The news of a large-scale “return to the office” for workers has not been making much headway, as employees enjoy the flexibility provided by remote and hybrid work. 2024 benefits are projected to reflect those needs.

According to the same Mercer report, at least 80% of companies surveyed allowed the option for some employees to regularly work from home.

Hybrid or generally flexible work hours may allow your team to complete tasks at their own pace, which increases productivity. This way, location becomes less important and employers can prioritize results over hours in the office. The use of tools that support remote work for those working from home has also seen a resurgence in the past few years.

3. Expanded opportunities for PTO

Employee expectations for time out of office are moving far beyond standard PTO. In 2024, companies will allow more opportunities for time off related to mental health and caregiving needs. Inclusive PTO policies help destigmatize mental health-related absences and can help protect employees from losing pay when faced with unexpected circumstances.

These paid time off options include parental, adoption and paid surrogacy leave. Even unlimited vacation policies are gaining traction, which can encourage employees to take time off without the constraints of a set number of days. In 2021, the majority (72%) of employers with unlimited PTO policies reported that the amount of time off employees took was the same as it was under their prior policy.

Also, according to the Mercer report, about one in four employers provide unlimited PTO to at least some employees and the threshold for taking time off has increased. The median number of paid time off provided increased to 7 weeks among companies surveyed in the Mercer report.

4. Reproductive and caregiving benefits

Reproductive health will also see a spotlight in 2024. Employers are looking to expand healthcare coverage to include fertility treatments, family planning resources and maternity and paternity leave policies. Scheduling flexibility can also be a boon for working parents, along with subsidized care or resources.

Common caregiving benefits include child care consultations, subsidized child care services and special needs support. Currently, some employers surveyed by Mercer offer specialized benefits for high-risk pregnancy (31%), preconception family planning (32%), post-partum (24%) and more. According to the Mercer report, 46% of employers will offer one or more of these benefits in 2024, up from 37% in 2023.

Employees get to take advantage of a variety of programs that are beneficial to their specific situation. Companies will see increased support for caregivers as a vital tool for recruitment and talent retention. The future of caregiving benefits will consider the many needs of employees, and prioritize a wide-ranging plan regardless of gender or family structure.

Give your 2024 employee benefits strategy an edge and offer financial wellness tools from Best Money Moves.

Best Money Moves is a mobile-first financial wellness solution designed to help dial down employees’ most top-of-mind financial stresses. As an easy-to-use financial well-being solution, Best Money Moves offers comprehensive support toward any money-related goal. With 1:1 money coaching, budgeting tools and other resources, our AI platform is designed to help improve employee financial well-being.

Whether it be retirement planning or securing a mortgage, Best Money Moves can guide employees through the most difficult financial times and topics. We have robust benefits options for employers, regardless of their benefits budget.

Our dedicated resources, partner offerings and 700+ article library make Best Money Moves a leading benefit in bettering employee financial wellness.

To learn more about Best Money Moves Financial Wellness Platform, let’s schedule a call. Contact us and we’ll reach out to you soon.