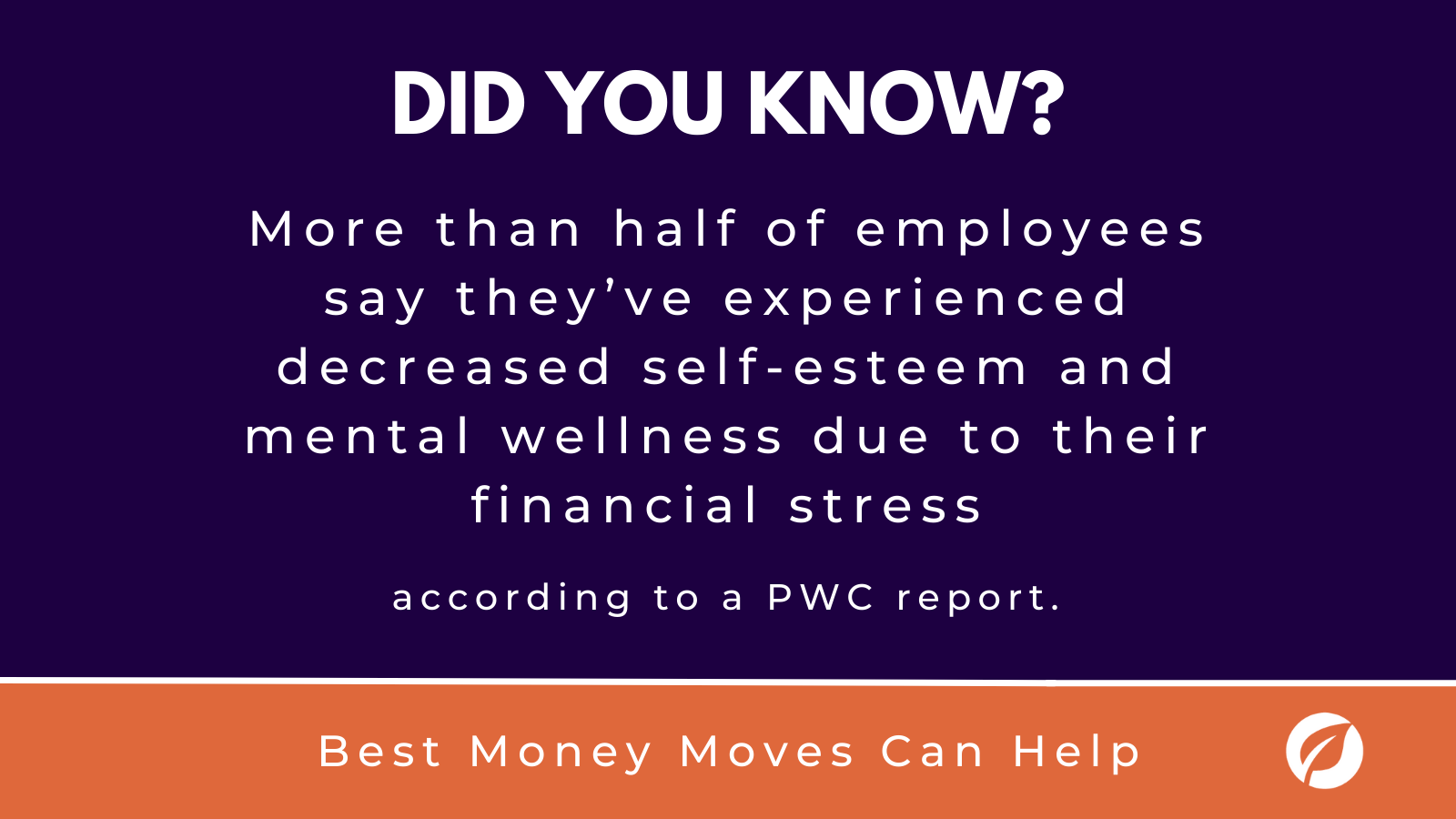

Best Money Moves Sneak Peek: Are your employees financially stable? Get a special inside look into the resource library of Best Money Moves.

Whether your employees need help with day-to-day budgeting, debt management, planning for their financial future or something in-between, our resource library can help. Best Money Moves users have access to over 900 unique articles, videos, webinars and calculators across a range of financial topics. Users at any point of their financial journey can find the guidance they need when they need it most.

Enjoy a sneak peek of a user-favorite Best Money Moves article: 10 questions to determine if you’re financially stable

Lots of moving pieces factor into your financial stability. Whether you’re trying to save, building a budget, planning for retirement or otherwise handling your money, it’s easy to get overwhelmed. However, there are questions you can ask to make sure you’re on the path toward financial stability — and steps to take if you’re not quite there yet.

1. Do you keep a budget?

Setting a fixed budget is the first step toward responsible spending. List your income and your expenses so you clearly see where to cut costs and save each month.

Start by listing the total income you bring in each month, including your salary, a spouse or partner’s salary and other recurring income such as alimony or childcare. Then, compare this income to an itemized list of your expenses. It’s helpful to split your list into “fixed” expenses that stay constant every month (rent, car payments, etc.), and varied costs (entertainment, clothes). By splitting necessary costs from everything else, and keeping track of what you spend money on, you can better learn your spending habits and find places to reduce unnecessary spending.

2. Do you think through big purchases?

Patience is important when it comes to spending. While it’s easy to buy on impulse, splurging can result in purchases outside of your budget. When making a big purchase — whether a large appliance, a vacation or even a home — compare your options to find the best value.

3. Do you put money into savings every pay period?

Saving is key to long-term financial stability. Building a savings ensures you’ll be prepared for whatever emergencies life throws your way. Even if you only put away a small amount each month, these savings will grow over time.

To guarantee you save, try having your bank automatically transfer part of each paycheck to a savings account. If your bank isn’t able to do so, check with your employer to see if they can automatically deposit some of your paycheck into a savings account instead.

4. Do you have enough savings to cover three months of expenses?

According to the Federal Financial Literacy and Education Commission, you should have enough savings to cover three months of expenses before you start making any other investments. Our recommendation is to save closer to six months’ worth of expenses, but three months is a great place to start building your savings over time.

Regardless of your overall goal, if you have enough in savings to last you at least a few months, it likely means you’re in a healthy place financially and don’t have to stress about breaking your budget when an unexpected expense arrives. For more in-depth information on building an emergency fund, read our article How do I build an emergency fund?

5. Do you know what your credit score is and how to keep it in good shape?

Your credit score reflects your history of borrowing and paying back money and is comprised of a variety of factors, including your current unpaid debt, your history of paying bills and your total number of credit accounts. Banks and other lenders use your credit score to determine the likelihood that you’ll repay a loan on time. A high credit score means you’ll likely have an easier time qualifying for a mortgage, credit card or other forms of credit.

Many credit card companies or banking apps offer their customers a free monthly credit score, usually found on your monthly statement or by logging into your bank account’s mobile application. It’s important to note, however, that these free scores are generally educational scores and may be several points off from your actual score. Alternatively, you can purchase a copy of your credit score from each of the three nationwide credit bureaus Equifax, Experian and Transunion.

Keep your score in good shape by paying your loans on time, not getting close to your credit limit and only applying for the credit you need and know you can pay back.

6. Do you have an established credit history?

Having an established history of using credit will help you with your credit score. The more often you pay your loans on time, the better your score will be and the better your chances are at receiving loans in the future.

If you do not have experience with credit yet, the Consumer Financial Protection Bureau recommends looking into products designed to help you build credit. There are several options — such as secured credit cards and credit builder loans — that were created to kickstart your credit history.

7. Do you have alerts set up for your checking accounts?

Setting up alerts for your checking accounts is an easy way to avoid overdraft fees. Overdraft fees occur when you don’t have enough money in your account to complete a purchase, but the bank allows the transaction to go through anyway. Alerts on your account will tell you when you are low on money. This is important because, even if you’ve recently made a deposit, your funds may not be immediately accessible, which means that you can still overdraw your account and end up paying fees.

Be proactive and set alerts to ensure you’re always aware of how much money you have access to at a given time.

8. Do you plan for your tax refund?

Financial stability is often contingent on financial planning, and having a plan for your tax refund can help you reach or maintain financial stability.

Estimate how big your refund will be based on how much you earn, and then create a plan for its best possible use. Whether you put it into savings or use it to catch up on bills, planning ahead will help you make the most of your refund.

To really plan ahead, put down your savings account and routing numbers when you file your taxes. This way, the IRS can deposit your check directly into savings so there’s no temptation to spend it right away.

9. Do you have long-term financial goals?

It’s always healthy to have long-term financial goals. Having realistic, specific goals can help you stay on track with your spending. This concrete planning for the future motivates you to save and gets you to where you want to be financially.

10. Are you planning for retirement?

It’s never too early to start planning for the future, especially if you’ve reached a point where you can save money every month. A retirement fund may seem daunting or too far off to worry about, but contributing to one regularly can help you save up over time.

The amount needed for a comfortable retirement varies from person to person, but a general rule is that you will need 70% of your current annual salary. However, if you plan on being very active in retirement, this number may be higher.

If you haven’t started thinking about retirement yet, start by establishing an Individual Retirement Account (IRA) through your bank or other financial institution. An IRA is an account that allows you to save money for retirement with tax-free (or tax-deferred) growth. By keeping retirement in the back of your mind, you’ll ensure your financial stability lasts long after you stop working.

Managing your finances may seem difficult at first, but there are many simple steps you can take to help you become more financially stable.

Best Money Moves gives your employees access to a detailed library of 900+ financial articles, videos, webinars and other tools.

Best Money Moves is a mobile-first financial wellness solution designed to help dial down employees’ most top-of-mind financial stresses. As a comprehensive financial well-being solution, Best Money Moves offers 1:1 money coaching, budgeting tools and other resources to improve employee financial well-being. Our AI platform, with a human-centered design, is easy to use and fit for employees of any age.

Whether it be retirement planning or securing a mortgage, Best Money Moves can guide employees through the most difficult financial times and topics. Our dedicated resources, partner offerings and 700+ article library make Best Money Moves a leading benefit in bettering employee financial wellness.

To learn more about Best Money Moves Financial Wellness Platform, let’s schedule a call. Contact us and we’ll reach out to you soon.