Financial Wellness Is The Best Answer To Wage Stagnation

For millions of American workers, the income from one job is simply not enough to cover basic living expenses anymore. Despite an increase in prices and growing inflation, wages have remained unchanged for many Americans. According to ResumeNow’s Wage Reality Report, one-third of workers say their salary hasn’t kept pace with inflation, and it’s taking a major toll on financial health, mental health and productivity.

Because compensation is failing to keep pace with rising costs, companies are pivoting to financial wellness programs to provide solutions both employers and workers desperately need.

Learn why Financial Wellness may be the best answer to this growing issue.

Who Suffers From Wage Stagnation?

Wage stagnation happens when workers’ pay increases at a slower rate than inflation, reducing their ability to afford common goods and services. Wage stagnation has become increasingly common across the United States, with 55% of workers reporting their salaries are lower than they should be.

The consequences of wage stagnation go far beyond tight household budgets and savings accounts. According to a survey from Zety, more than one in three workers feel hopeless, anxious or frustrated about their chances of meeting life goals on their current salary. This financial distress directly impacts workplace performance, with 36% of employees reporting feeling less motivated to exceed expectations at work.

Even more concerning for employers, more than one in four workers are actively seeking new job opportunities for higher salaries. Meanwhile, 20% admit they’re more focused on increasing their income than improving their job performance.

The Hidden Cost of Financial Stress

The impact of wage stagnation directly affects a company’s bottom line. Financial stress costs employers an estimated $200 billion annually through decreased productivity, increased absenteeism and higher turnover rates.

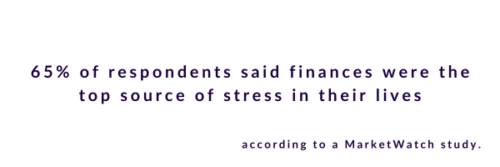

This stress affects employees of all levels. According to Forbes, 76% of C-suite executives and HR leaders reported experiencing financial stress themselves, while a staggering 92% of employees acknowledged being stressed about their finances.

While financial stress affects employees in the short term, long term financial milestones are also stunted. According to HR Dive, 40% of employees say they cannot save for retirement, while 37% report being unable to afford to buy a home.

In response to these challenges, organizations are using benefits packages to provide financial wellness initiatives. These initiatives address immediate needs while building long-term financial resilience among their workforce.

Financial wellness programs typically include:

- Educational resources that help employees better manage their existing finances

- Retirement planning support that helps employees prepare for the future regardless of current wage constraints

- Comprehensive budgeting tools that help track and manage expenses

- Personalized AI insights for specific employee needs

Why Financial Wellness Is the Key to Addressing Wage Stagnation

While wage stagnation presents significant challenges for both employees and employers, financial wellness programs offer a practical path forward even when salary increases aren’t feasible. These initiatives address the core issues behind financial stress while providing employees with tools to support existing compensation and build toward more secure futures.

By investing in financial wellness, companies can significantly reduce the productivity drain caused by financial stress while demonstrating a commitment to employee wellbeing. This approach creates a more engaged, productive workforce and builds loyalty during a period when more than a quarter of financially stressed workers are contemplating leaving for better opportunities elsewhere.

The data is clear: when companies can’t immediately solve wage stagnation through compensation increases, comprehensive financial wellness programs offer the most effective alternative for empowering employees and creating financially healthy organizations.