3 Impacts of Employee Student Debt in 2024

After a three-and-a-half-year forbearance period, federal student debt payments resumed in October of 2023. Depending on the individual, student debt can pose anything from a minor headache to a crippling financial hurdle that delays other milestones for years to come.

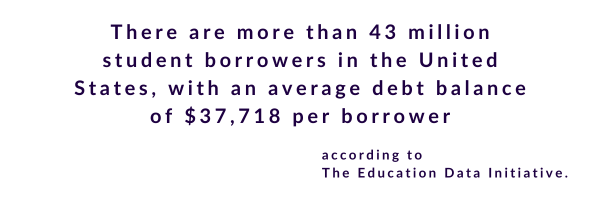

The Education Data Initiative estimates that there are more than 43 million student borrowers in the United States, with an average debt balance of $37,718 per borrower. So, more likely than not, at least some members of your team were affected by the loan restart. Keep an eye out for these three ways that employee student debt may impact your team in 2024.

1. Financial stress from employee student debt negatively impacts employee mental health.

1. Financial stress from employee student debt negatively impacts employee mental health.

The average monthly employee student debt payment for graduates is about $500, according to more data from the Education Data Initiative. It takes almost 20 years for people to fully pay off their debts. Borrowers are expected to fit these monthly expenses alongside existing financial responsibilities. But for many employees, especially those living paycheck-to-paycheck, that can be easier said than done. Paying an extra hundreds of dollars per month can be backbreaking and often leads to an increase in financial stress.

In a recent Education Trust report, 64 percent of graduates surveyed said that student debt negatively impacted their mental health. And this stress isn’t uncommon even among high earners. According to CNBC15% of workers earning $100,000 say they still live paycheck to paycheck.

An increase in financial stress generally leads to reduced productivity as well. A recent PwC survey found that more than 50% of workers spend three hours or more per week at work dealing with issues related to their finances.

2. Employee student debt may delay other financial milestones.

The reintroduction of employee student debt payments also may delay financial milestones. Goals like saving for retirement, purchasing a home or building an emergency fund can be delayed or even gutted due to the pressure for additional monthly payments.

According to a Bankrate survey, around 60 percent of U.S. adults who currently struggle with student loan debt have put off making important financial decisions as a result.

Delaying financial milestones can drastically affect a person’s mental health, as they are forced to forego life-changing events (such as getting married or having children) due to financial strain. The same Bankrate study found that 57 percent say their quality of life has been negatively impacted by the economy. Postponing milestones can also affect an employee’s earning power. Without the ability to receive more education due to debt, employees are stuck with lower-level jobs and the difficulty of trying to get a new degree or certification.

3. Employees juggling student debt may face career setbacks.

Graduates who struggle with student loans often need to postpone additional education or training while they work on their debt. This may stagnate potential career growth and limit the opportunities employees may have to excel at their jobs.

Financial stress can also impact performance at work, as a SHRM survey found that these issues have resulted in a 34% increase in absenteeism and tardiness.

In fact, employees who aren’t reaching their financial goals often decide to take initiative and find new jobs altogether. According to the ADP Research Institute, employees who consider their student loan debt to be a “heavy burden” are 2.4 times more likely to be in the process of leaving their organization.”

In conjunction with this is the issue of job satisfaction. Almost one in five employees say that their jobs are not doing enough to support their financial goals. Whether it’s not making enough to support themselves or being unable to save for any sort of emergency expense, employees are often left with questions regarding their financial future.

Addressing employee student debt head-on

Although the student loan crisis is dire, there are still ways employers can help curtail the negative effects of student loans to keep their workforce thriving and happy.

Financial Wellness Initiatives

- Financial wellness programs are some of the most effective ways to address the issues student loans create. Debt can be difficult to understand and can seem impossible to navigate for first-time borrowers. But these programs empower employees to take control of their debt and their financial futures. Financial wellness initiatives go beyond traditional benefits, as they focus on teaching financial literacy with topics like budgeting, saving, and managing debt.

Tuition Reimbursement

- A key benefit for employees in 2024 will be a comprehensive tuition reimbursement program. Some companies allow their employees to use earnings as a way to pay off student debt, similar to a 401(k) plan. Others use a simple recurring payment option as an incentive for employees. A direct repayment program can ease the burden of student loans and allow workers to focus on their financial milestones without feeling set back.

Luckily, 74% of workers who are stressed about money actively seek help during an important financial decision, whether it’s from their employers or online resources. Creating a space where employees can learn about financial wellness effectively is one of the greatest boons you can give to your workforce. Through budgeting tools, educational resources and personalized recommendations, these programs allow employees to take control of their financial lives.

To learn more about Best Money Moves Financial Wellness Platform, let’s schedule a call. Contact us and we’ll reach out to you soon.