Here Are The 4 Important Insurance Terms Gen Z Employees Need To Know

sssThe 4 Important Insurance Terms Gen Z Employees Need To Know. Gen Z employees often struggle to understand common insurance terms. Learn about how employers can help with financial wellness benefits.

Insurance is a complex topic, no matter how experienced you are. However, Gen Z employees are suffering from a lack of knowledge of insurance terms and policies. In fact, only about a quarter of Gen Z adults could define the terms “deductible” (27%) and “copay” (29%) when surveyed National Association of Insurance Commissioners (NAIC). Around 35% said they could define “out of pocket.” Just 19% said they understood the term “out-of-network.”

Engaging with insurance is key to developing a strong sense of financial security. You can accrue significant savings from the right health, auto or renters policy. This may prevent many Americans from taking on crippling debt.

Here are the top insurance terms your Gen Z employees should know and why they matter.

ssThe Top Insurance Terms Your Gen Z Employees Should Know

Open Enrollment is when employees can sign up for, adjust or change their health insurance policies. It is vital for employees to understand when this period starts and ends, in order to be prepared if they (or someone in their family) get sick. Reviewing their plan may also expand their ability to receive prescription drugs and specialized care for certain illnesses.

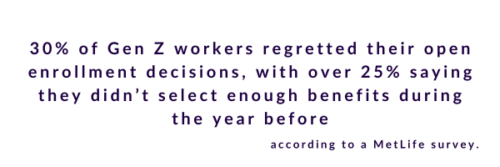

A MetLife survey found that 30% of Gen Z workers regretted their open enrollment decisions. Over 25% said they didn’t select enough benefits during the year before. In fact, nearly half of Gen Zers said they waited too long before choosing benefits. 53% said they didn’t even understand what was being offered.

A deductible is the amount of money an individual pays (per year or per condition) before insurance companies begin covering any expenses. A copay is a similar fixed payment that occurs each time an individual sees a doctor. A premium represents the actual cost of an insurance plan, dictating the amount a person pays to keep their plan active.

According to WorkLife, only 60% of Gen Zers understand these three insurance terms and can explain how they relate to their coverage. Confusion surrounding insurance often causes people to turn to unreliable sources for help, which can lead to uninformed decisions. Defining insurance terms helps employees to make the most out of their healthcare benefits.

Financial education bridges the information gap

In order to support your younger employees, insurance education must be transparent and personalized to each individual. To ensure your employees understand their insurance policies, include financial wellness into your benefits program.

A financial wellness program offers educational resources that gives your team the best chance to succeed. Their pressing questions about insurance, open enrollment and other guidance are packaged into simple, easy-to-understand articles and videos.

It’s clear that financial education, especially surrounding insurance, is vital for your employees’ success. Whether your workforce is fresh out of college or preparing for retirement, the help they need is readily available if your focus targets their financial wellness needs.

Best Money Moves is a mobile-first financial wellness solution designed to help dial down employees’ most top-of-mind financial stresses. As an easy-to-use financial well-being solution, Best Money Moves offers comprehensive support toward any money-related goal. With 1:1 money coaching, budgeting tools and other resources, our AI platform is designed to help improve employee financial well-being.

Whether it be retirement planning or securing a mortgage, Best Money Moves can guide employees through the most difficult financial times and topics. We have robust benefits options for employers, regardless of their benefits budget.

Our dedicated resources, partner offerings and 1000+ article library make Best Money Moves a leading benefit in bettering employee financial wellness.

To learn more about Best Money Moves Financial Wellness Platform, let’s schedule a call. Contact us and we’ll reach out to you soon.