Financial Resiliency: The Skill You Didn’t Know Your Team Needed

Financial resiliency: The skill you didn’t know your team needed. Learn why fostering financial resiliency may be key to a more productive, confident workforce.

Everyone encounters rough financial patches at some point. The key is how easily you adapt to these challenging. situations. This concept is at the core of financial resiliency, the skill your workforce may be missing.

Financial resiliency refers to a person’s ability to withstand life events that impact their income, assets, or overall financial wellness. Divorce, sudden medical issues and unemployment can throw a wrench into a person’s finances. However, the right tools and support can help employees build financial resiliency and weather any storm.

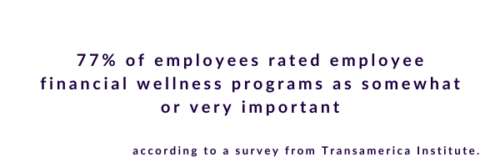

Employees often look to their employer as a source of financial wellness support. In a survey of nearly 2,000 employees conducted by Transamerica Institute, seventy-seven percent of respondents rated employee financial wellness programs as somewhat or very important. Yet only 28% of employers report offering such benefits to their teams.

Supporting employee financial resiliency can help companies dial down employee financial stress and accelerate the path to financial security. Learn more about the unique benefits of a financially resilient team. Plus, learn to build resiliency among your organization at large.

1. Many employees cannot afford a $1000 emergency

Having enough money for a rainy day is a key pillar of financial resiliency. According to Bankrate’s 2024 Emergency Fund report, nearly 1 in 3 employees have $0 saved for emergencies — a clear indication of low financial resiliency. If faced with a $1000 emergency, many Americans would have to borrow the money, whether through a loan, from a family or friend, or carrying a balance on their credit card, according to Bankrate’s report.

To help employees craft a more financially resilient future, consider offering an emergency fund as part of your employee benefits package. One practice is to have employees complete financial wellness courses/training in exchange for a $1000 emergency fund — this benefit offering demonstrates a keen dedication to building employee financial resilience and education.

2. Looming debt can impact employees’ financial resiliency and overall health

Debt can come from a myriad of sources — car loans, education, payday loans, medical expenses, and more. Regardless of one’s debt origins, high levels of debt can lower one’s financial wellness and ability to withstand future financial emergencies.

Having a high debt-to-income ratio can limit the options an employee has amid a sudden emergency, even for employees earning six-figure salaries. Lenders and banks may view individuals with a high debt-to-income ratio as high-risk borrowers — this can lead to extremely high interest rates or being denied for a loan altogether. With high interest rates, carrying debt has become increasingly expensive. Over time, the chronic stress from carrying debt can also take a toll on the human body.

According to Forbes’ Mental Health & Debt survey, about 40% of Americans reported experiencing anxiety due to debt-related stress, and nearly half reported having trouble sleeping due to debt-related stress.

3. Help employees build financial resiliency using personalized financial wellness tools

High levels of debt can make borrowers feel stuck and unsure about the best way to manage their looming debt. Moreover, looming debt can feel cyclic.

Employees don’t have to manage their financial stress alone. A robust financial wellness program can empower employees along their financial wellness journey and help them build financial resiliency.

Every employee has a different starting place when it comes to financial wellness and. Find a financial wellness program that personalizes their offerings and counseling, based on each employee’s unique situation, as opposed to taking a cookie-cutter approach. This can help equip employees with the right tools and resources to develop financial resiliency for today and years to come.

Best Money Moves is a mobile-first financial wellness solution designed to help dial down employees’ most top-of-mind financial stresses. As an easy-to-use financial well-being solution, Best Money Moves offers comprehensive support toward any money-related goal. With 1:1 money coaching, budgeting tools and other resources, our AI platform is designed to help improve employee financial well-being.

Whether it be retirement planning or securing a mortgage, Best Money Moves can guide employees through the most difficult financial times and topics. We have robust benefits options for employers, regardless of their benefits budget.

Our dedicated resources, partner offerings and 1000+ article library make Best Money Moves a leading benefit in bettering employee financial wellness.

To learn more about Best Money Moves Financial Wellness Platform, let’s schedule a call. Contact us and we’ll reach out to you soon.