5 Surprising Symptoms of Financial Stress (And 5 Helpful Solutions)

5 surprising symptoms of financial stress (and 5 helpful solutions). The effects of financial stress can be devastating to your workforce. Learn what to look out for and how you can make a difference.

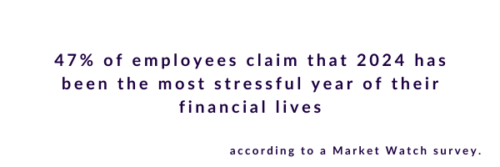

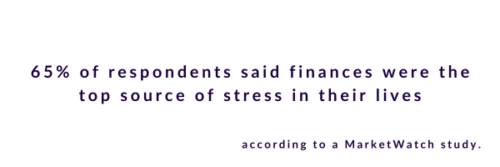

Employee financial stress was in the spotlight throughout 2024 amid continued inflation and economic uncertainty. In a survey of 2,000 Americans, MarketWatch found that 88 percent of respondents reported feeling some form of financial strain. 65 percent felt that finances were the top source of stress in their lives.

By now, it’s clear that employee financial stress is a significant issue. However the way that stress manifests often comes as a surprise to employers.

The Qualified Plan Advisors’ 2024 Financial Wellness Survey found that 68 percent of the American workforce experiences financial stress. Both mental health and sleep are the most negatively impacted, though personal relationships and physical health are also significantly affected by financial stress.

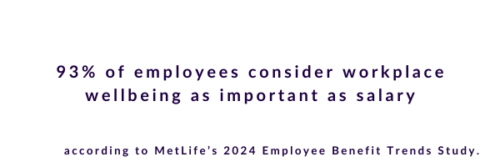

Over 70 percent of employees agree or strongly agree that their employers have a responsibility to ensure employees remain financially well. Furthermore, nearly 70 percent of employees prioritize job opportunities that offer financial wellness programs.

Here are five of the most surprising symptoms of financial stress that could be impacting your workforce — along with five helpful solutions to help keep your workforce financially healthy.

1. 31% of employees with financial stress report a deterioration in mental health.

Financial struggles that arise from worrying about debt or the inability to pay for basic necessities can lead to stress. According to TIAA Institute researchers, these struggles lower the ability to deal with mental health challenges. High debt levels are associated with anxiety, depression and anger. Ongoing financial struggles can contribute to feelings of hopelessness and despair that can culminate in depression.

One way employers can help is by providing access to mental health resources. Programs include counseling services, employee assistance and mental health workshops. Employers can also help create a supportive workplace culture where mental health is discussed openly.

2. 31% of employees struggle with sleep disturbances.

Financial worries can also manifest in sleep disturbances, resulting in decreased energy levels. These financial worries may be a result of the high debt levels seen among employees. QPA’s survey found that 80% of employees carry debt, primarily in the form of mortgages, credit cards and student loans. 64% of individuals lack adequate emergency funds.

Employers can help mitigate this symptom by addressing financial stress at its root through bespoke debt management tools. Providing budgeting worksheets and money management apps help employees grasp financial essentials.

Employers can also organize education sessions focused on bolstering financial literacy on topics. Offering tools is only the first step; ensuring employees know how to use them is crucial.

Additional benefits might include student loan repayment assistance, matching debt contributions and flexible work arrangements. These help employees save on commuting costs or enable them to work multiple jobs to pay off debt.

Employers can also provide educational sessions on the importance of sleep as well as how to establish healthy sleep routines. Encouraging a balance between work and life helps employees both manage their time and improve their sleep quality.

3. 18% of stressed employees indicate challenges in their relationships.

Honesty about money is crucial to maintain healthy relationships. Employers should provide financial guidance that looks at money as a part of a person’s overall life that becomes integrated into all relationships.

Learning how to allocate two paychecks, budgeting for household expenditures and discussing long-term savings and retirement goals can all help employees understand what they need from their relationships and move forward with effective money management.

Implement family-friendly policies such as maternity/paternity leave, childcare assistance and flexible working hours for both parents to ease both financial and emotion burdens, leading to healthier family dynamics.

4. Financial stress is linked to adverse physical effects for 11% of employees.

Physical health is just as important as financial health, and the two can go hand in hand. Focus on developing wellness initiatives that encompass financial, physical and mental health. Here, employees can access various wellness resources, from fitness programs and nutrition advice to financial planning tools and mental health support.

Offering regular workshops and seminars on financial literacy can be combined with health-related topics like stress management and nutrition. Physical wellness-specific initiatives can include on-site fitness classes, gym memberships or discounts at local fitness centers with participation encouragement through fitness challenges and rewards. Having healthy snacks and meals in the workplace and access to regular health screenings can also help employees stay on top of their physical health.

5. 9% of employees experience reduced work productivity as the result of financial stress.

The TIAA Institute found that financial stress resulted in a 34 percent increase in absenteeism and tardiness. Financially stressed employees are five times more likely to be distracted by finances while at work. QPA’s Financial Wellness Survey shows that 45 percent of Americans allocate one hour or more to manage their personal finances. Financially stressed employees also miss almost double the number of days as unstressed employees.

To help employees stay better focused at work, designate some working hours to set your workforce on the right track. Offering financial wellness programs in the workplace can help employees manage their finances better, reducing financial stress and improving productivity. These programs can include financial literacy workshops, coaching, and other resources.

Employers can also consider offering financial benefits such as retirement planning assistance and emergency savings funds. This way, allocated time is spent on productive financial educational opportunities, improving overall workplace productivity while giving employees the resources they need for financial success.

Best Money Moves is a mobile-first financial wellness solution designed to help dial down employees’ most top-of-mind financial stresses. As an easy-to-use financial well-being solution, Best Money Moves offers comprehensive support toward any money-related goal. With 1:1 money coaching, budgeting tools and other resources, our AI platform is designed to help improve employee financial well-being.

Whether it be retirement planning or securing a mortgage, Best Money Moves can guide employees through the most difficult financial times and topics. We have robust benefits options for employers, regardless of their benefits budget.

Our dedicated resources, partner offerings and 1000+ article library make Best Money Moves a leading benefit in bettering employee financial wellness.

To learn more about Best Money Moves Financial Wellness Platform, let’s schedule a call. Contact us and we’ll reach out to you soon.