4 Things You’re Missing About Employee Financial Stress

When it comes to employee financial stress, employers and employees aren’t always on the same page.

In their 2023 Financial Wellness in the Workplace Report, PNC surveyed over 1,000 U.S. full-time workers across various organizations about employee financial wellness. When surveyed, 80% of employers felt their teams were at least somewhat financially prepared for the future – but only 50% of employees felt the same way.

If you’re looking to create a happier, more financially secure workforce, don’t overlook these 4 insights from PNC about the impacts of employee financial stress.

1. Employees don’t have long-term financial security.

Despite feeling secure in their jobs, around 63% of all surveyed employees still live paycheck to paycheck, according to PNC data. These workers face unique challenges when it comes to paying down debt and saving for future financial goals. Employees living paycheck-to-paycheck can’t build emergency savings and are more susceptible to relying on credit cards and loans in the face of unexpected expenses.

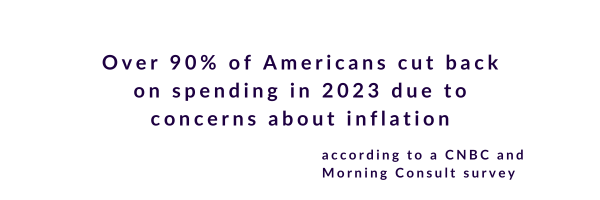

What’s more, employees are still feeling the effects of an uncertain economy. Ninety percent of employees report being negatively impacted by inflation with 81% finding it more difficult to put money into savings. Three out of every four employees worry that there will be a recession in the near future.

2. High-earners aren’t immune to employee financial stress.

While it may seem like employee financial stress is only an issue for young or economically disadvantaged employees, that’s simply not the case. Employees of all ages and income levels are feeling the weight of financial challenges. Of the surveyed employees who made $100,000 or more per year, fifty-seven percent still report feeling somewhat or very stressed about their financial situation. The numbers are even more severe for employees at lower income levels. For employees earning $50,000 to $99,999, 77% report the same financial challenges. For employees earning less than $50,000, the numbers jump to 79%.

3. Employee financial stress impacts performance on the job.

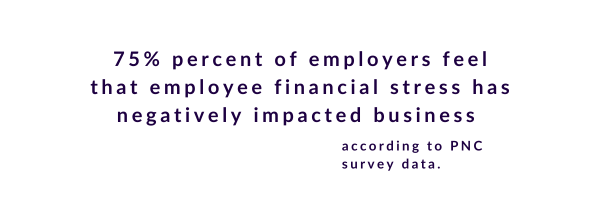

Employee financial stress has tangible consequences for a business’s bottom line. Eighty-seven percent of employees surveyed by PNC admit to thinking about their financial situation while on the job. On average, employees report spending three hours per week worrying about money. This distraction hasn’t gone unnoticed by employers — 75% percent feel that employee financial stress has negatively impacted business in the form of reduced productivity (39%), unhappy employees (18%) and overall poor performance outcomes (16%).

4. Employees expect their employers to take an interest in their financial well-being.

When asked for their opinion on solutions to target employee financial stress, 80 percent of respondents said they would stay longer with an employer who offered financial wellness benefits. Younger employees are especially anxious for this help, with 88 percent of respondents 21 to 34 years of age more likely to stay with a financially conscious employer.

Likewise, 96% of employers say financial wellness benefits positively impact retention. However, although employers agree that these benefits pay off, many still offer the bare minimum. Many will offer retirement matching but don’t include additional benefits such as financial counseling and education. Financial wellness benefits are a great way to help your company stand out amongst competitors when attracting and maintaining your workforce.

Best Money Moves is an interactive financial wellness benefit that helps employees make smarter choices about their money.

Whether employees are building their first budget, paying down debt, working toward homeownership or planning for retirement – Best Money Moves has the tools they need to turn financial goals into reality.

Schedule a call with a member of our team to learn more about Best Money Moves. Contact us and we’ll reach out to you soon.