3 ways high inflation is still affecting your workforce. Learn how to help your team cope with the continuing effects of high inflation.

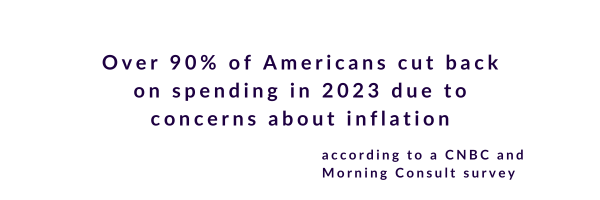

Although inflation cooled during the end of 2023 and price increases have somewhat slowed, most employees aren’t feeling the benefits of a recovering economy. Over 90% of Americans cut back on spending in 2023, according to a CNBC and Morning Consult survey, due to the effects of rising inflation. Going into 2024, many of these reduced spending habits are expected to remain as 88% of respondents still listed inflation as a top concern.

Find out how inflation and high prices may still be affecting your employees. Plus, learn more about the actionable solutions that your team can use to help employees find relief from financial stressors.

3 ways high inflation is still affecting your workforce

1. Employees increasingly use “buy now, pay later” services to cover grocery expenses

Between supply chain disruptions and rising consumer demand, prices for most household goods have risen at historic rates. Americans are struggling to keep up with new market prices. So much so that, employees are turning to “Buy Now, Pay Later” services to pay for household expenses, according to research by Adobe Analytics.

After paying rent or mortgage payments and car payments, some Americans don’t have any cash left to cover all of their monthly expenses. So, to help make ends meet, many are turning to buy now, pay later services and apps, a form of short-term financing that allows shoppers to take out an easily accessible loan at checkout that they then repay in installments over time.

Initially, Buy Now, Pay Later services were used to help individuals finance large expenses, such as a new treadmill or computer, and repay the borrowed amount in installments. However, today, many cash-strapped employees have resorted to buy now, pay later services to pay for their groceries and other necessities.

Using installment loans to cover day-to-day purchases is a short-term solution at best. At worst, it leaves buyers vulnerable to mounting debt, missed payments and even credit score damage.

2. Inflation-fueled gas prices continue to eat into employees’ monthly budgets

Although national gas prices are lower than they were a year ago, according to the AAA, employees still struggle to afford new gas prices. And amid supply-and-demand issues and geopolitical tensions, gas prices remain susceptible to price volatility.

Similar to groceries, to help afford gas prices, employees are increasingly taking out loans and buy now, pay later accounts to cover expenses. This means that instead of using today’s dollars to pay for gas, employees are increasingly relying on future dollars and digging themselves into a potential cycle of debt.

3. Employees put fewer dollars toward their retirement savings.

To prioritize and balance expenses, many employees have turned their financial focus away from the long-term, and become laser-focused on the short-term. The impact of inflation has fueled many employees to stop saving for retirement, and instead, spend that money on short-term necessities.

About 25% of employed adults decreased their retirement savings in 2022 and 12% stopped saving altogether, according to a TIAA report. Among Hispanic and Black employees, the percentage is disproportionately higher.

Many employees are making sacrifices today that impact their future financial standing. However, with the right financial wellness tools, employees can learn how to balance near-term financial responsibilities with long-term financial goals.

How companies can help their employees amid financial uncertainty

1. Offer robust budgeting tools

Balancing multiple expenses every month can be challenging, but with a robust budget tool, employees can keep track of monthly and one-off expenses all in the same place. Whether it be utility bills or entertainment expenses, keeping track of spending habits and categories can help employees improve their financial practices over time.

2. Establish flexible retirement plans and resources.

Retirement planning tools and calculators can help employees balance current financial responsibilities while preparing for tomorrow’s goals. With the right tools, employees can learn prepare for retirement, despite the ups and downs of the economy. For instance, if an employee regularly contributes 10% of every paycheck to retirement savings, when economic hardship hits, financial planning calculators can help employees gauge a new contribution percentage that works for their latest financial situation.

3. Invest in financial wellness advisors and workshops

Some employees are aware of inflation and economic uncertainty; however, they’re unsure of how these economic events connect to them and affect their financial standing. With a financial advisor, employees can get personalized financial guidance and understand how today’s economic events impact them. In addition, consider hosting financial wellness workshops on topics that resonate with employees in your workforce. For instance, if many employees are interested in homeownership, consider a workshop on how interest rates impact mortgages.

Offset the strain of inflation with comprehensive employee financial wellness

Best Money Moves is an interactive financial wellness benefit that helps employees make smarter choices about their money.

Whether employees are building their first budget, paying down debt, working toward homeownership or planning for retirement – Best Money Moves has the tools they need to turn financial goals into reality.

Best Money Moves users gain access to a suite of debt trackers, budgeting calculators and a library of 900+ articles, videos and webinars. Our tools empower employees with actionable solutions to real-world problems. Best Money Moves users also receive exclusive member deals from our library of trusted benefits partners, including discounts on insurance, college planning prescription medications and so much more.

Schedule a call with a member of our team to learn more about Best Money Moves. Contact us and we’ll reach out to you soon.